Let’s delve into the fascinating world of petroleum and its products, specifically focusing on the United States, while also considering the global market. We will provide a wealth of information, utilizing charts, graphs, and other relevant data release dates to break it down into manageable parts.

So where do we begin? The US Energy Information Administration (EIA) reported that in 2021, the US consumed an estimated 19.89 million barrels of petroleum per day, amounting to a total of 7.26 billion barrels for the year. (Source: Link)

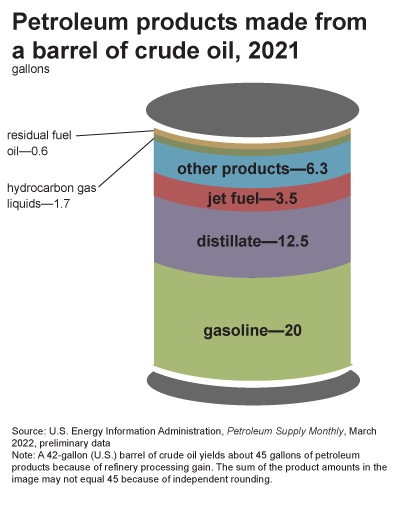

While most people associate petroleum with gasoline, diesel, and jet fuel, the truth is that it plays a much more significant role in our daily lives than we might realize. Petroleum-based products include saline bags for hospitals, makeup products, rust-protection coatings, colors, paint, candles, furniture sealing agents, and even food products such as mineral oil.

Petroleum has become an essential component of modern life, present in everything from the screen you are currently reading to the fuel that powers your car. In this article, we will examine the current state of petroleum production and consumption in the United States. We will specifically focus on the production and consumption of oil, and in future articles, we will delve deeper into the impact of gasoline prices on our daily lives.

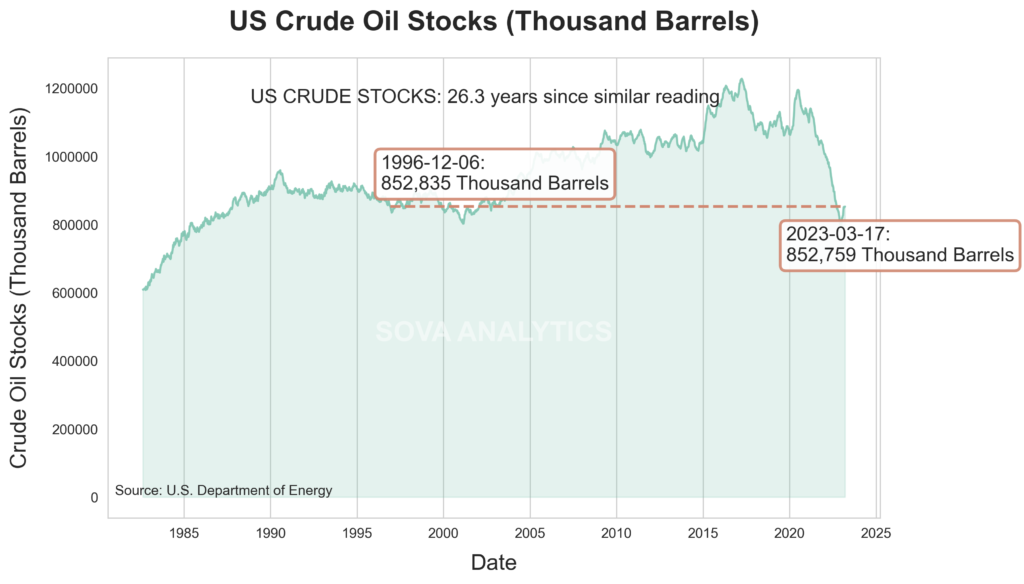

US CRUDE STOCKS

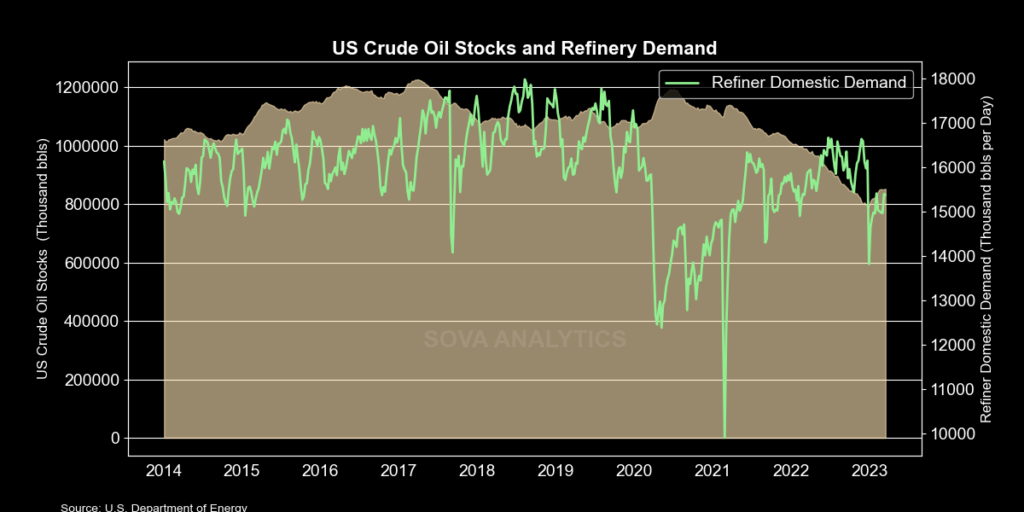

The petroleum industry has been severely impacted by the global pandemic and ongoing conflict in Eastern Europe, leading to a significant decline in available global oil stocks. To counter this, the US has increased its crude oil exports. While recent reports indicate that oil stocks are starting to recover, it’s important to note that the current stock levels are only at the same level as in 1996. Furthermore, the previous week, the US experienced stock levels that haven’t been seen since the 1980s, which is a cause for concern.

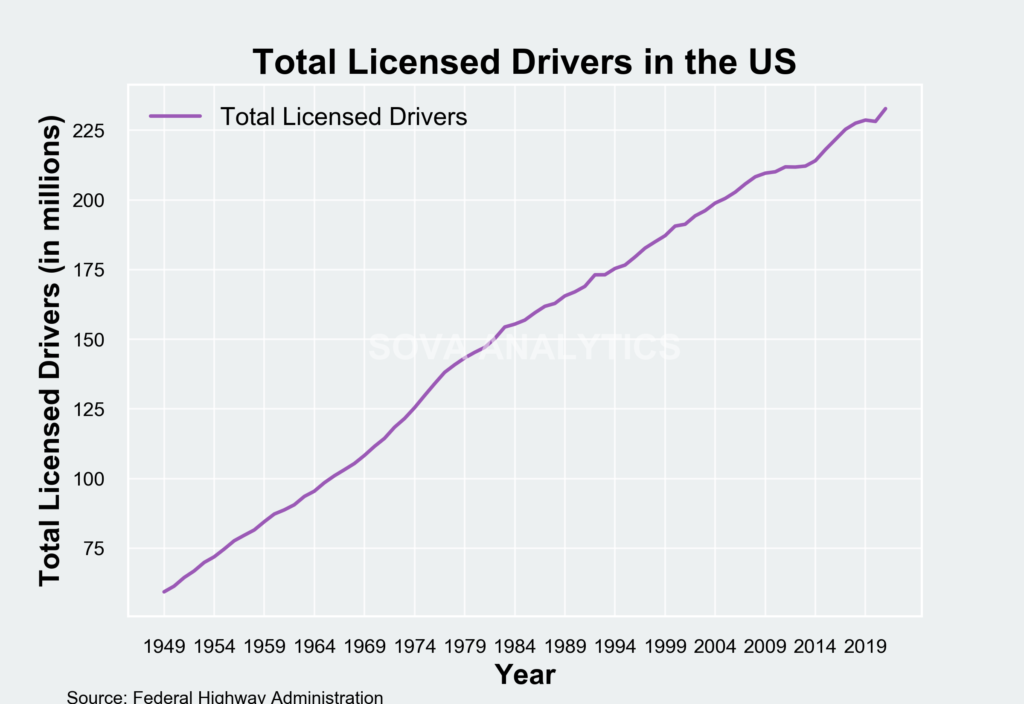

This situation is particularly alarming as the number of US drivers has increased by over 30% since 1996, yet there is less crude available for refining. This disparity could result in higher prices for consumers and potentially impact the overall economy. It’s crucial that the petroleum industry continues to closely monitor and adjust to these trends to avoid any adverse effects on the market.

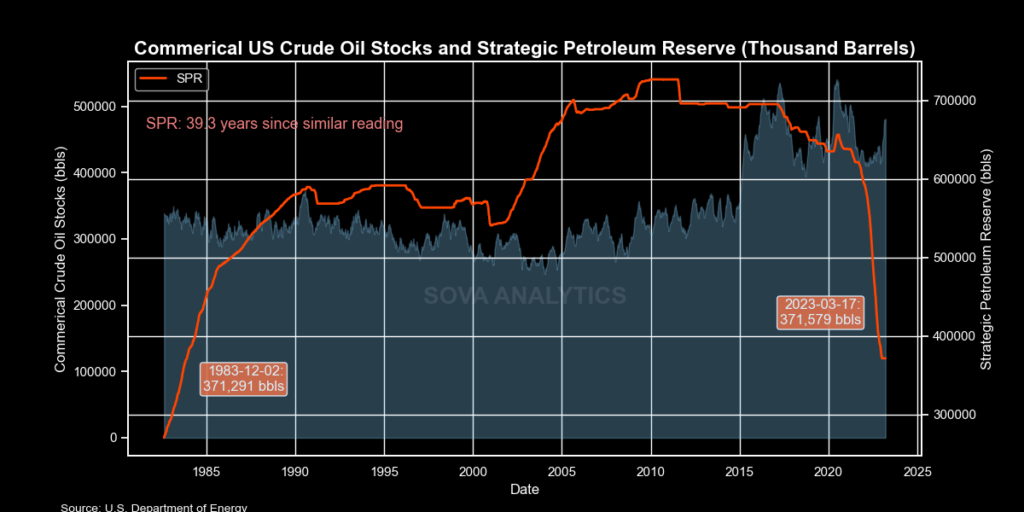

Crude oil stocks are affected by a range of factors, including production, consumption, imports, and exports. When the supply and demand for oil are out of balance, there may be either a surplus or a deficit of inventory. To address this, the US maintains a Strategic Petroleum Reserve (SPR), which serves as a crucial safety net. The SPR enables the US to access its reserves during emergencies or to store excess supply, ensuring a stable and reliable supply of petroleum for the nation.

The US Department of Energy (DOE) states that the Strategic Petroleum Reserve (SPR) is the largest emergency oil stockpile globally, with a current storage capacity of 713.5 million barrels of crude oil (DOE, 2022) The SPR consists of four underground storage sites situated along the Gulf of Mexico coastline in Texas and Louisiana. As of the end of 2022, the SPR held around 372 million barrels of crude oil.

The SPR was established in 1975 in response to the Arab oil embargo, which caused significant supply disruptions and price hikes in the US (EIA, 2021). The SPR’s main objective is to provide a cushion against supply disruptions and price shocks, ensuring that the US has adequate reserves to sustain its economy and security during emergencies.

Strategic Petroleum Reserve

Crude oil stocks in the US consist of two primary components: commercial stocks and the Strategic Petroleum Reserve (SPR). The SPR has experienced continuous releases to the open market, leading to a decline in its volume to levels not seen since 1983. This has caused concerns about its effectiveness in safeguarding the US economy and security during emergencies. Plans to refill the SPR when prices are lower face several challenges that we will explore.

On the other hand, commercial stocks are held by private sector companies, such as oil refineries, traders, and marketers, to meet their operational needs. These “working stocks” are continuously used and replenished as necessary. Although they play a crucial role in the overall crude oil supply chain, their availability can be affected by demand, production, and prices.

The United States has emerged as a major force in the global oil market, reaching a milestone in 2019 by becoming a net exporter of crude oil and petroleum products for the first time in almost 70 years. This development has significant implications for the US oil industry, which now has the opportunity to meet the increasing global demand for energy. However, it is crucial for the industry to balance the needs of both domestic and global markets while ensuring the effectiveness of the Strategic Petroleum Reserve (SPR). In the following section, we will explore the issue of crude oil exports and their impact on the US oil industry.

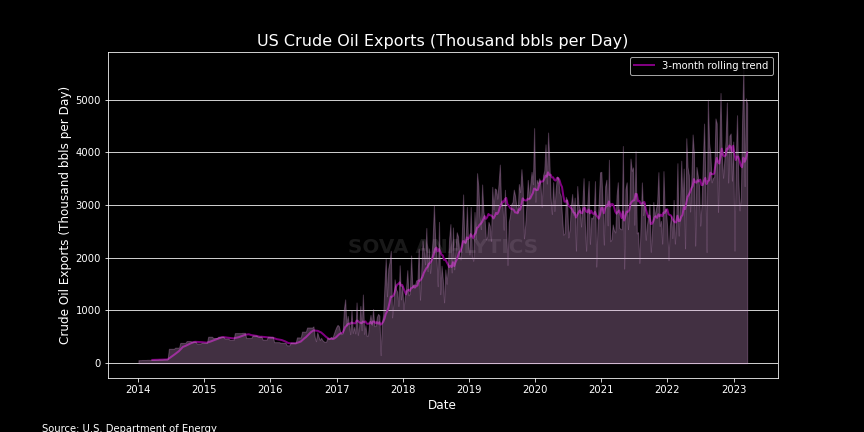

US Crude Exports

In response to the oil crisis of the 1970s, the US government banned the export of crude oil in 1975. This ban remained in place for over 40 years until it was lifted in 2015 by the Obama administration. The law allowing for the export of crude oil was seen as a significant policy shift that aimed to capitalize on the country’s newfound energy abundance and to reduce reliance on foreign oil sources.

Since then, US crude oil exports have been steadily increasing, with record-breaking numbers seen in recent years. The US has become one of the world’s top oil exporters, with shipments to various countries, including China, South Korea, and India. The growth in exports has been attributed to the country’s abundant shale oil resources, improvements in drilling technology, and the lifting of the export ban.

Since the lifting of the crude oil export ban in 2015, exports have been steadily increasing. In 2022, there was a significant surge in exports due to the impact of the Ukraine war on the global crude oil supply chain. This surge resulted in several days in 2023 where exports exceeded 5 million barrels per day, marking some of the highest levels of exports in US history.

It’s worth noting that the increase in exports has also led to benefits for the US economy, including job creation, increased revenue, and reduced reliance on foreign oil sources. Nonetheless, it’s crucial to ensure that the benefits of exports are balanced with the need to maintain adequate crude oil stocks for domestic use and emergency situations. The complex nature of the global oil market and its impact on US energy security require a well-coordinated approach that considers all aspects of the supply chain.

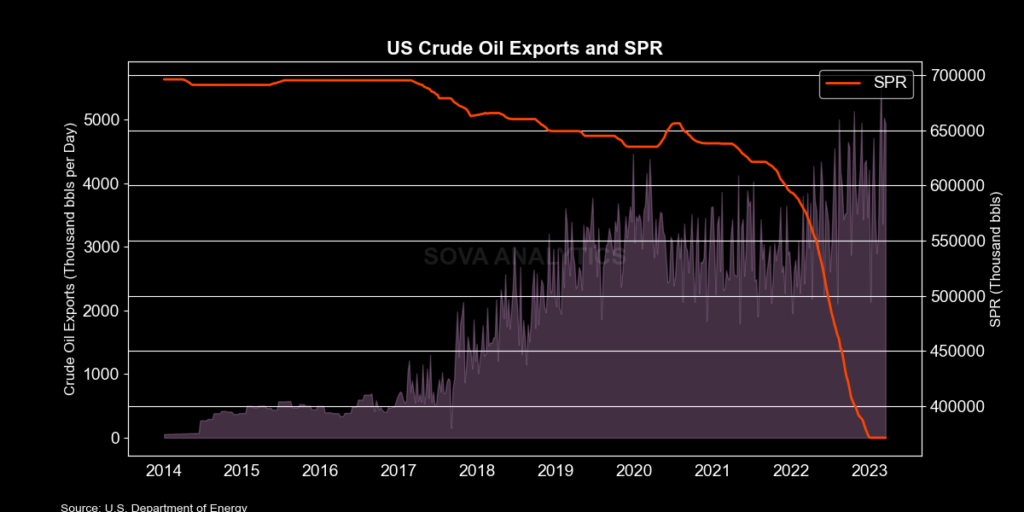

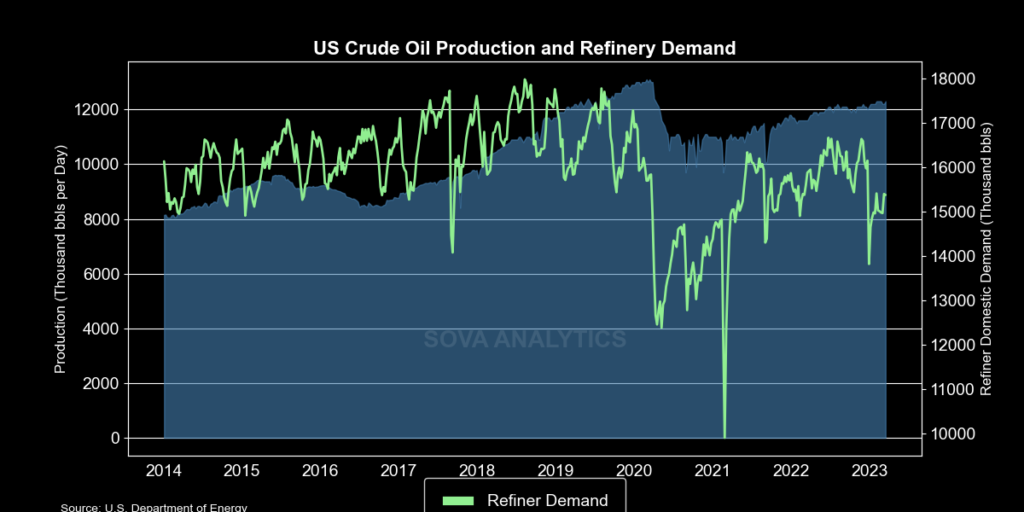

The chart displayed above illustrates a clear correlation between the rise in exports and the decline in the Strategic Petroleum Reserve (SPR) volume. While some of the exports can be attributed to the SPR release, it is important to note that not all of them came from the reserve. After experiencing a contraction due to the pandemic, US oil production has begun to recover in 2022. The US Energy Information Administration (EIA) projects that crude oil production will continue to increase, with an anticipated average of 12.4 million barrels per day in 2023, setting a new record.

Despite the increase in US oil production, a considerable portion of it is being utilized by domestic refiners. While some of it is being exported, a significant amount is being used domestically. According to the EIA, US crude oil refinery inputs averaged 15.9 million barrels per day in 2022, which represents a 5% increase from the previous year. This rise in refinery inputs has played a vital role in meeting the surging demand for petroleum products in the US, including diesel, gasoline, and jet fuel.

Amid concerns about the stability and security of the US crude oil supply chain, some have suggested halting exports to refill the Strategic Petroleum Reserve (SPR). However, such a decision requires careful consideration of its potential impact on global oil markets and the global economy.

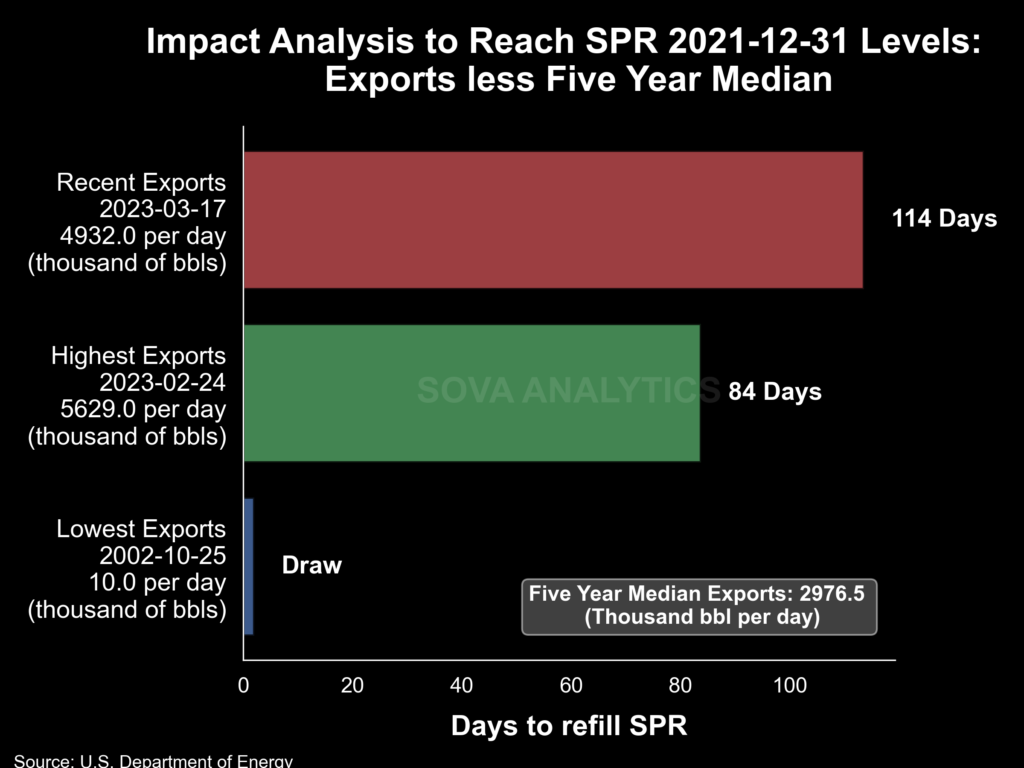

To assess the feasibility of this approach, we conducted a thorough impact analysis that took into account a range of factors that could affect global supply levels. Our analysis focused on the time required to refill the SPR, assuming a reduction in current US crude oil exports to the 5-year median level.

Based on our findings, we estimate that reducing current US crude oil exports to the 5-year median level would take approximately 114 days to refill the SPR. However, it’s important to note that this estimate assumes that the current international buyers of US oil would be able to find additional supply globally, which is not guaranteed.

The US was one of the world’s largest crude oil exporter in 2022 with an average of 3.5 million barrels per day (b/d) of crude oil exports according to the US Energy Information Administration (EIA). Recent data shows that in the past 30 days, US crude oil exports have increased by over 47% compared to the 2022 average, indicating that the world may be becoming more reliant on US crude exports. While the stability and security of the US crude oil supply chain have been a concern, halting exports to refill the Strategic Petroleum Reserve (SPR) could have far-reaching impacts on global oil markets and the global economy. Any major disruptions in the supply chain or significant changes in demand could result in a shortage of oil in the global market, leading to increased oil prices and potentially a humanitarian crisis.

US Refinery Demand

The role of exports in balancing domestic crude oil supply and demand in the US market is crucial. However, limited access to global markets can pose a challenge for oil-producing regions in the US, necessitating the use of pipelines, trucks, or rail for transportation. Loading facility capacity and ship availability can also affect export quantities. Despite these challenges, exports continue to play a vital role in balancing the domestic supply and demand of crude oil in the US market.

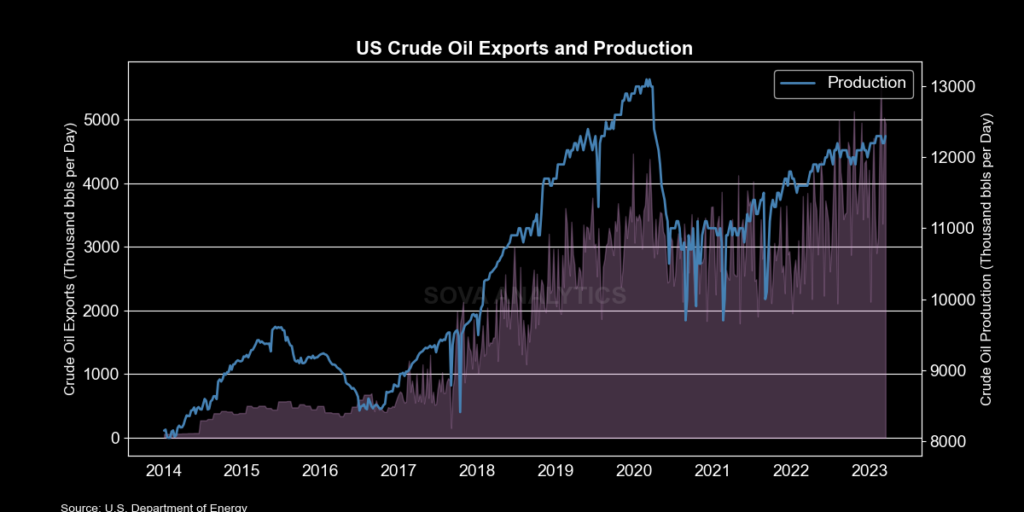

As demonstrated in the chart above, the pandemic-induced reduction in US refinery demand caused a decline in crude production as refineries processed less oil to produce products like gasoline, diesel, and jet fuel. Nevertheless, crude oil production continued to increase due to increased exports, while refinery demand remained stable at around 15-16 million barrels per day. This underscores the critical role of exports in balancing the domestic crude oil market.

US refinery demand also is a important item to consider in crude oil stocks. According to the US Energy Information Administration, as of June 2022, the US had 130 operating refineries with a total refining capacity of 17.9 million barrels per day. Refineries transform crude oil into various products, including gasoline, diesel, and jet fuel, which are in high demand both domestically and globally.

The demand for these refined products is affected by a variety of factors, such as seasonal changes, economic growth, and government regulations. For instance, during the summer months, demand for gasoline tends to increase as more people travel, while in the winter months, demand for heating oil tends to rise.

Refinery demand also has a direct impact on crude oil production. During the pandemic-induced decline in demand, crude production was reduced as a result of the lower demand for refined products. Similarly, when refinery demand is high, crude production tends to increase to meet the demand for feed stock.

Moreover, refinery demand can influence crude oil exports, with refineries sometimes prioritizing supplying the domestic market over exports. This can affect the overall balance of supply and demand in the US crude oil market, as excess crude oil may need to be stored or exported to other countries.

In 2021, the resurgence in refinery demand caused crude stocks to diminish, as the recovery of domestic crude production was slower. This, in turn, resulted in an upswing of imports to meet the demand for oil products that were not being met by domestic crude production, along with releases from the Strategic Petroleum Reserve (SPR).

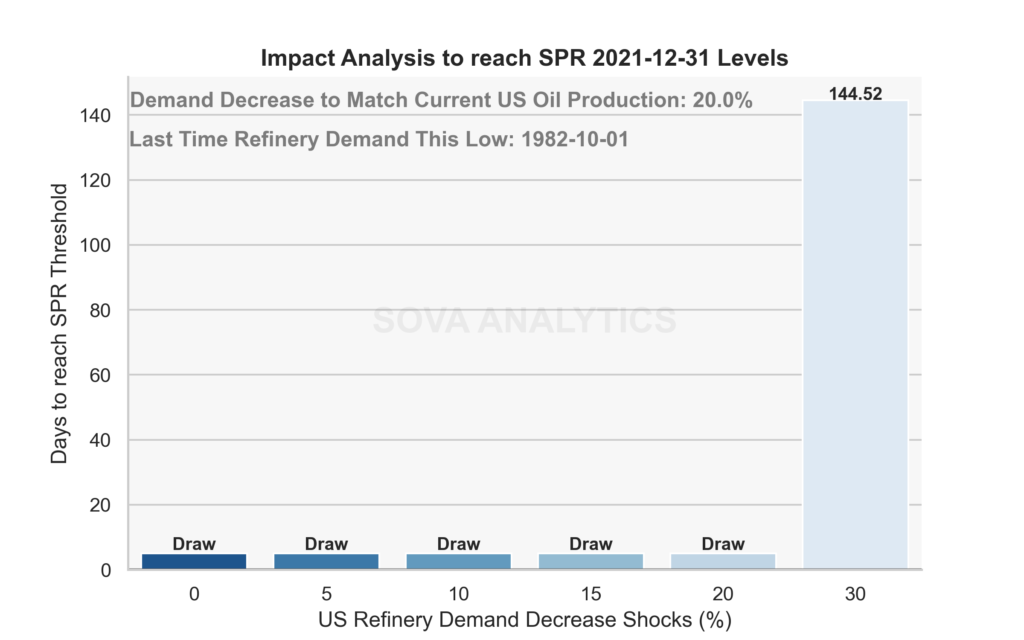

To replenish the SPR to early 2022 levels, one proposal is to decrease domestic refinery demand. However, our impact analysis has revealed that this would require a substantial reduction in US crude oil demand, exceeding 20%. Specifically, cutting refinery demand by 30% would take approximately 145 days and necessitate a drop in demand similar to levels not seen since 1985.

Alternatively, increasing imports to make up for the shortage in domestic production is another option, but it warrants careful evaluation of its implications. Import source considerations should include geopolitical repercussions. Furthermore, it is crucial to weigh the cost-effectiveness of importing oil versus producing it domestically.

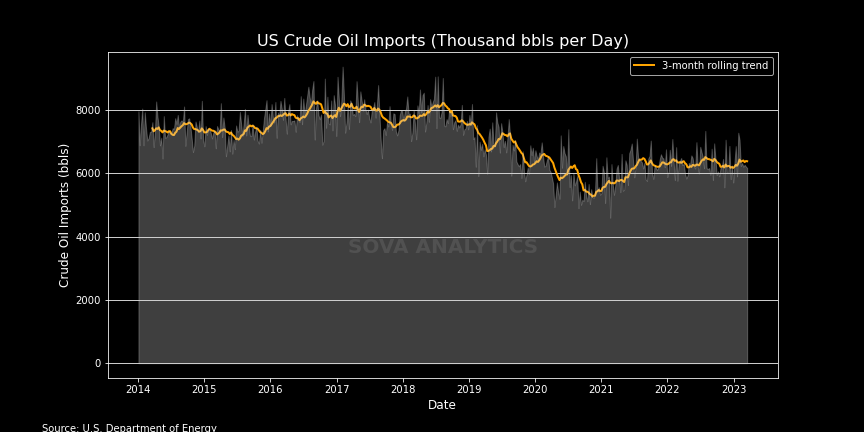

US Crude Imports

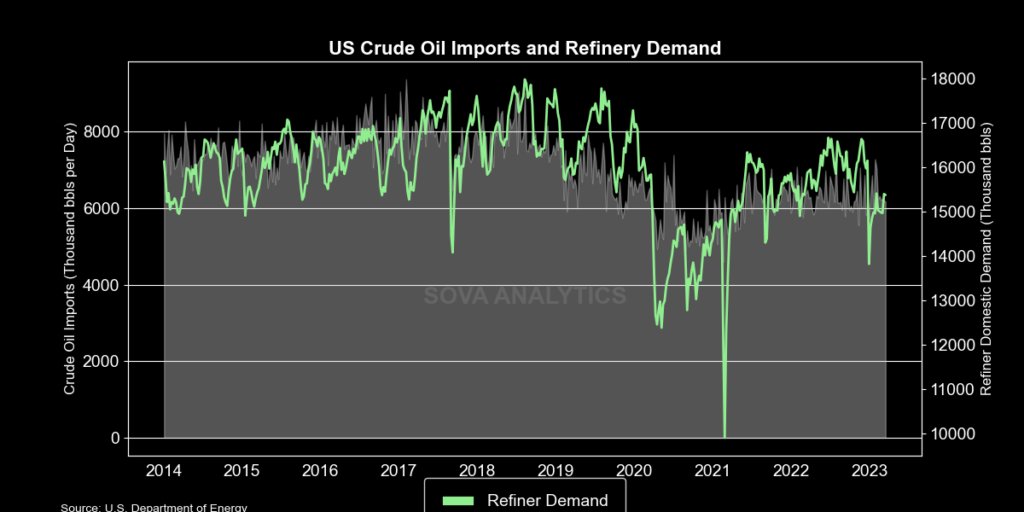

In early 2021, imports increased to meet the rising refinery demand, with data showing that imports of crude oil averaged around 6 million barrels per day during that period. Since then, imports have remained stable at that level, even as refinery demand continues to rise. However, there has been a historical slow decline in imports, which is in line with the increasing domestic production and exports of crude oil that the US has seen in recent years.

As per the US Energy Information Administration (EIA), the US crude oil imports peaked at 10.1 million barrels per day in 2005. However, with the advent of advanced drilling technologies, such as hydraulic fracturing, US domestic production has surged, reducing the country’s reliance on foreign oil. Consequently, US crude oil imports have been on a steady decline, falling to 6.8 million barrels per day in 2020, a decline of approximately 33% since 2005. This reduction in crude oil imports has had significant impacts on the US economy, including increased energy security and reduced trade deficits.

The COVID-19 pandemic disrupted the global oil market, causing an unprecedented decline in demand for crude oil and petroleum products. The US crude oil imports were also severely affected, dropping below the 3-month trend line as a result of the pandemic-induced demand shock, lock downs, and travel restrictions. As the economy started to recover and refinery demand picked up, imports began to rise again, indicating that the US was still reliant on foreign crude to meet its energy needs. The most recent data suggests that US domestic production and refinery output have caught up with domestic demand, and imports have fallen below the trend line once more.

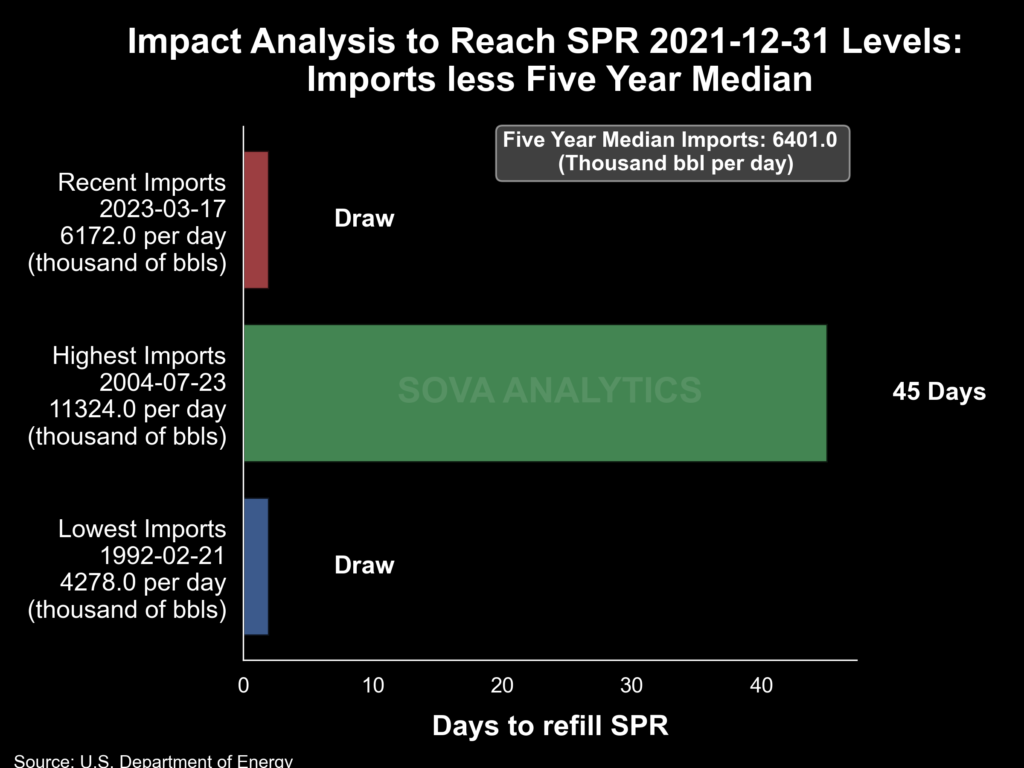

As previously discussed, one potential solution to increase the Strategic Petroleum Reserve (SPR) is to increase oil imports. However, an impact analysis of current imports at different points in US history shows that the current import level of around 6 million barrels per day would not be sufficient to meet historical demand. Moreover, increased imports could make it operationally challenging to export crude at the same levels. The highest level of oil imports ever recorded was in 2004, with over 11 million barrels imported. Even assuming the current five-year median import requirements, it would still take around 45 days to refill the SPR back to its December 31, 2021 levels. This would likely require a reduction in exports to accommodate the increased imports.

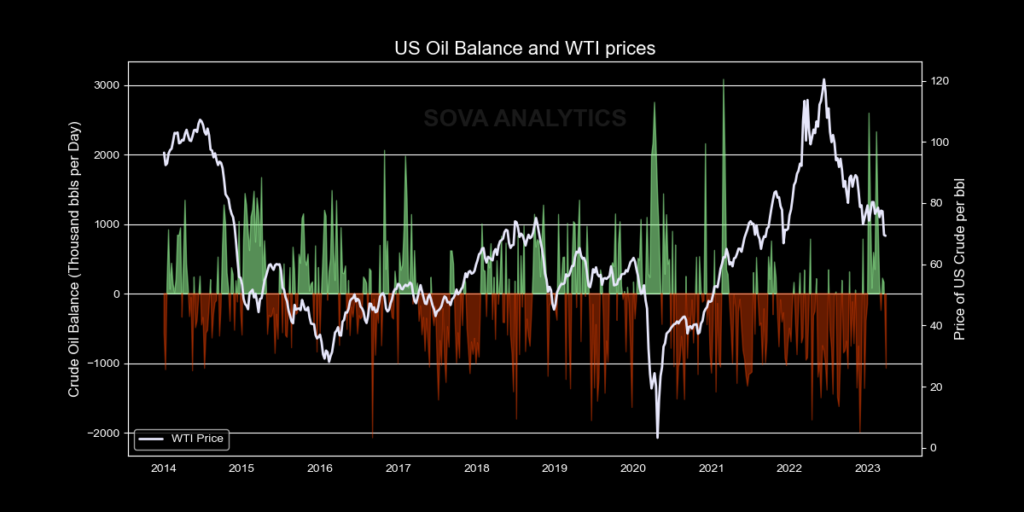

US Crude Balance

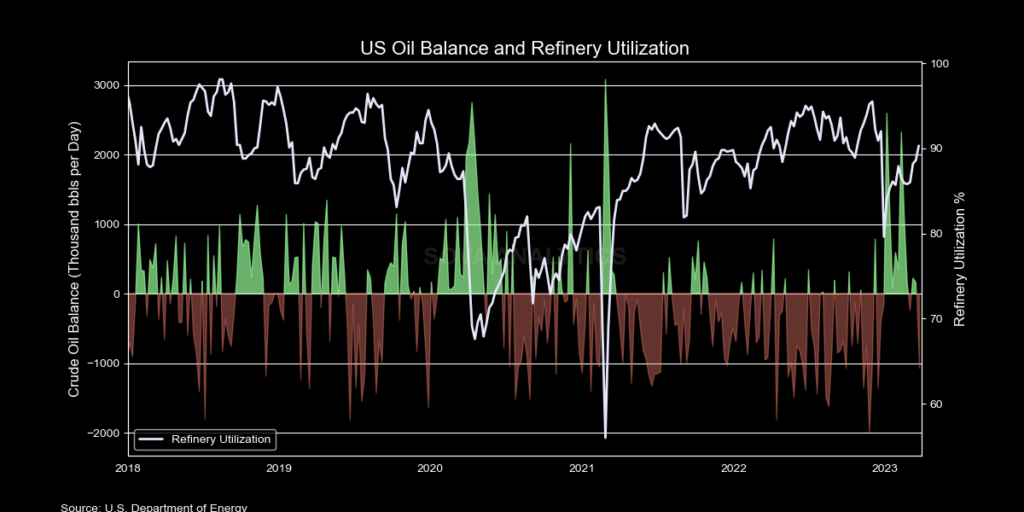

The US oil market is a complex system that requires close attention to key metrics such as production, imports, exports, and refinery consumption. One crucial metric that plays a critical role in understanding demand for crude oil and the production of refined products is refinery utilization.

Refinery utilization is a measure of how much of a refinery’s capacity is being used to refine crude oil into products such as gasoline, diesel, and jet fuel. In other words, it is a measure of the percentage of a refinery’s production capacity that is being utilized at any given time.

Refinery utilization is an important metric because it is directly linked to the demand for crude oil. When refinery utilization is high, it indicates that refiners are producing a significant amount of refined products and that there is strong demand for crude oil. Conversely, when refinery utilization is low, it may indicate weaker demand for refined products and lower demand for crude oil.

The utilization rate of refineries can vary depending on factors such as the level of demand for refined products, the availability of crude oil, and the profitability of refining operations. Refiners can adjust their utilization rates to match market conditions, and therefore, utilization rates can be a leading indicator of changes in the oil market.

In the US, refinery utilization is closely monitored by industry analysts, policymakers, and investors. Refinery utilization data is reported by the Energy Information Administration (EIA) on a weekly basis, providing an insight into the current state of the oil market.

Moreover, refinery utilization is a key factor in determining the oil balance of the US. The oil balance refers to the difference between the country’s oil supply and demand or “change in stocks”. When the US oil balance shows a surplus, measures such as lower exports, increased imports, lower refiner demand, or Strategic Petroleum Reserve (SPR) releases can be employed to address the imbalance. Conversely, when there is a deficit in the oil balance, exports can be increased, and the SPR can be replenished to address the shortfall.

The chart presented above indicates that an increase in refinery demand leads to a negative crude balance, while a decrease in refinery production results in a positive crude balance as depicted by the green bars. The current scenario is different as both refinery demand and exports are increasing, leading to a draw in crude balance. It is essential to note that there were builds in early 2023 when refiners reduced their demand and we appear to be seeing that trend reversing.

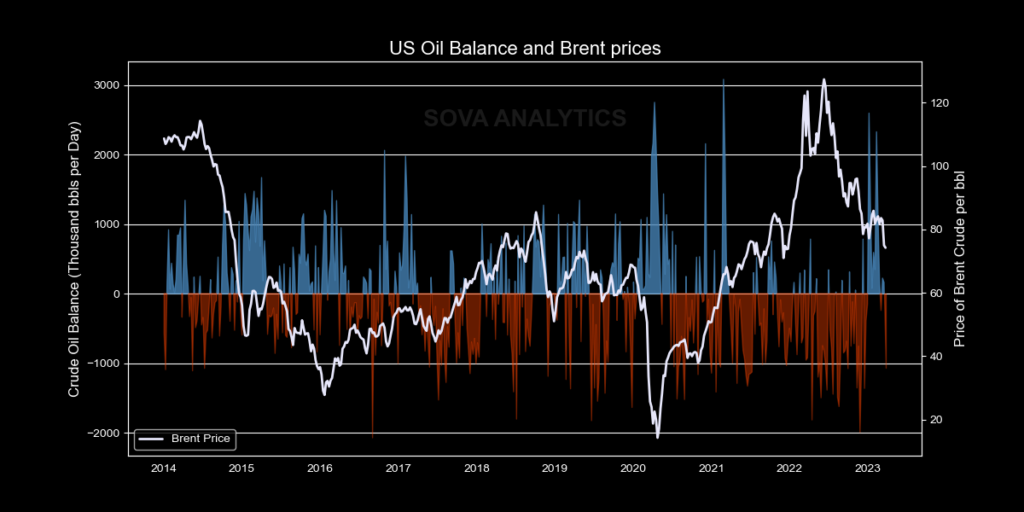

Additionally, the relationship between oil prices and the US oil balance was examined by Sova Analytics using the Brent international oil price index due to the significance of exports for the United States. It is crucial to note that prices are influenced by various factors; however, the chart clearly indicates that prices consistently increased when the US oil balance remained negative, and prices generally decreased when the US oil balance became positive. This emphasizes the importance of balancing the US oil balance to maintain stable prices and avoid significant price increases that can have adverse impacts on consumers and the economy. Therefore, it is crucial to consider multiple factors, such as geopolitical events and global supply and demand, to make an accurate prediction and effectively manage prices.

Summary

In summary, we have studied the various factors that contribute to the complexities of the US crude oil market, such as imports, exports, and the strategic petroleum reserve, and how they impact the overall balance and prices. We will keep you updated with weekly reports on the latest changes and trends, and we invite you to follow us on social media for these updates.

Moving forward, we will delve into the refinery aspect of the industry and investigate the factors that influence gasoline prices, especially as we approach the summer driving season. We are grateful for your ongoing interest in Sova Analytics and are dedicated to providing you with valuable insights and information. Thank you for choosing us as your trusted source, and we look forward to sharing more insights with you in the future.